Sébastien Dessillons has been appointed head of development at BNP Paribas Cardif and joins BNP Paribas Cardif’s Executive Committee effective from 1 July 2026. As part of the transformation and development department, his mission will be to strengthen BNP Paribas Cardif’s position as a world leader in bancassurance partnerships by enhancing partner engagement, developing a value proposition that leverages the opportunities

offered by artificial intelligence and fostering innovative partnerships.

Sébastien Dessillons began his career in the public sector. He held several positions at the French Ministry of Economy and Finance, then in ministerial offices first with the Minister of Defense (2012-2014), and then with the Prime Minister (2014-2016), focusing on companies and industrial affairs.

He then joined the BNP Paribas Group in 2016, where he was responsible for the

coverage of a portfolio of major corporate clients. He later led the sector teams within the Group’s Corporate and Investment Banking division, first for Europe from 2019, then globally from 2023. In this role, he managed investment bankers specialized by economic sector and supported corporate and private equity clients in their strategic transactions, including M&A and related structured financing.

Sébastien Dessillons is a graduate of École Polytechnique (France) and is a Chief Engineer of the Corps des Mines (Paris).

BNP Paribas Cardif, the insurance company of the BNP Paribas Group, and the BCC Iccrea Group, the largest Italian cooperative banking group with 111 Credit Cooperative banks, today announced that BNP Paribas Cardif has acquired an additional 19% stake in the life insurance company BCC Vita increasing its total shareholding to 70%. The transaction falls within the framework of the agreements signed in 2023 and marks the natural evolution of a partnership that has already demonstrated solid foundations and strong results.

After BNP Paribas Cardif’s acquisition of 51% of BCC Vita, the two partners have jointly built an effective and distinctive bancassurance model, designed to meet customers’ evolving insurance needs. The additional

19% acquisition reflects a shared long-term vision and mutual trust that has been consolidated over time.

The BCC Iccrea Group network, strongly rooted throughout Italy, represents an effective distribution asset for BCC Vita, enabling it to deliver high quality insurance solutions to a broad and diversified customer base.

“This new milestone reaffirms our commitment to the BCC Iccrea Group and further strengthens BNP Paribas Cardif’s presence in the Italian life insurance market. Our partnership is built on a strong model that combines our ability to support the banking network with close collaboration between our teams and BCC Iccrea Group’s local network, helping us respond effectively to customers’ needs,” said Pauline Leclerc-Glorieux, Chief Executive Officer of BNP Paribas Cardif.

“This transaction is the concrete confirmation of the value of a strategic choice in which we deeply believe,” said Alessandro Deodato, Chief Executive Officer of BNP Paribas Cardif in Italy. “When we started the partnership in BCC Vita two years ago, we did it with a clear vision and with the intention of embarking on a stable and lasting path together. With this further acquisition, we reaffirm our long-term commitment to the BCC Iccrea Group, one of the pillars on which the growth of BNP Paribas Cardif in Italy is based”.

“We are particularly pleased with how we have launched our partnership with BNP Paribas Cardif, and today we are extending it to allow our 111 BCCs to continue offering their members and customers one of the most comprehensive and competitive ranges of products in the life insurance sector in Italy,” concluded Mauro Pastore, General Manager of the BCC Iccrea Group –.

“The development of this partnership, as set out in the agreements signed in 2023, demonstrates the soundness of the strategic plan we had devised in the interests of our BCCs, which will now have a longer timeframe to consolidate their relationships with their communities and establish themselves as a key point of reference in this sector too”.

Through this transaction, BNP Paribas Cardif reinforces its commitment to the Italian insurance market and bancassurance. It also confirms BCC Vita’s role as a strategic vehicle for business development in the life segment, thanks to the strength of the BCC Iccrea Group’s distribution network and to the daily collaboration to broaden the product offering, enhance the customer experience in an evolving market.

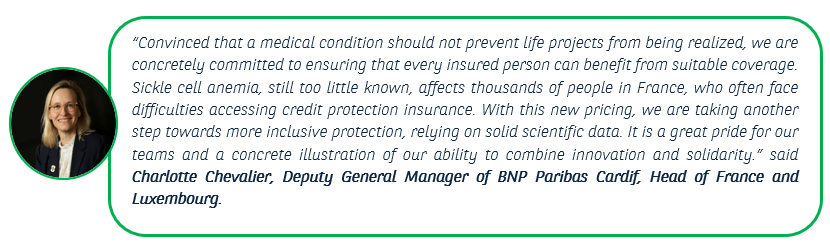

Building on its commitment to make insurance more accessible, especially for those affected by chronic or rare diseases, the insurer BNP Paribas Cardif is introducing new pricing for people with sickle cell anemia, the most common genetic disorder and the leading rare disease in France1. This advancement improves access to insurance in terms of coverage and pricing for creditor insurance contracts of BNP Paribas Cardif in France, both for clients of the BNP Paribas banking network and for brokers, wealth management advisors, and directly online via Cardif.fr

A significant step forward for the inclusion of people with sickle cell anemia

About 7.7 million people worldwide2 are affected by sickle cell anemia, a genetic disorder affecting red blood cells, representing a 40% increase in 25 years, including 30,000 people in France3. Those concerned often face difficulties accessing suitable credit protection insurance and are subject to premium surcharges on death and total and irreversible loss of autonomy guarantees, as well as significant exclusions on complementary guarantees, notably for work incapacity and disability.

Thanks to work carried out in collaboration with medical experts, BNP Paribas Cardif teams have developed a risk assessment that takes into account various therapeutic developments. This approach allows the insurer to improve pricing by more widely granting complementary guarantees and reducing surcharges. A new questionnaire is also introduced for insured people with sickle cell anemia to better understand the specifics of their condition.

When medicine advances, insurance evolves

Collaboration with the research community has enabled a better understanding of sickle cell anemia, its medical challenges, and its impact on patients’ quality of life. This initiative continues BNP Paribas Cardif’s actions for over 15 years to develop an inclusive offer, aiming to facilitate access to insurance solutions for people with rare or chronic diseases, such as inflammatory bowel diseases (IBD).

The insurer acts concretely to increase inclusion and access to creditor protection insurance. Among significant advances, BNP Paribas Cardif notably offers coverage without surcharge or exclusion to people treated for HIV, provided their viral load is undetectable at the time of subscription and to those who have overcome breast, prostate, or testicular cancer once the active therapeutic protocol is completed.

1Drépanocytose · Inserm, La science pour la santé

2 WHO issues first global guideline to improve pregnancy care for women with sickle cell disease [1] Épidémiologie de la drépanocytose en France et dans le monde | La Revue du Praticien

3 Épidémiologie de la drépanocytose en France et dans le monde | La Revue du Praticien

- Pre-tax net profit of 1.96 billion euros for full-year 2025, up 24% over 2024

- 40.5 billion euros in gross written premiums at end-2025, up 12% compared to 2024

- 302 billion euros in assets under management, up 6% compared to 2024

- 54% of gross written premiums with partners and networks outside the BNP Paribas Group

- Nearly 80 partnerships renewed or signed in 2025

- 52% of gross written premiums outside of France

These excellent results are the outcome of a unique partnership model deployed both within the BNP Paribas Group networks and with our external partners. The record gross written premiums in 2025 reflects the strength of our savings and protection activities, with strengthened positions in savings thanks to the solidity and quality of our euro fund in France and the successful integration of BCC Vita and Neuflize Vie. In line with our mission to make insurance more accessible, and with the renewed confidence of our partners, we are making it easier to subscribe and use insurance. We maintain high standards of customer experience by combining human interaction, digital tools, and artificial intelligence, adapting our insurance product coverage to societal changes, and facilitating access to insurance for vulnerable individuals.” commented Pauline Leclerc-Glorieux,

Chief Executive Officer of

BNP Paribas Cardif.

BNP Paribas Cardif reported pre-tax net profit of 1.96 billion euros in 2025, an increase of 24% compared to 2024. This performance was driven by the insurer’s dynamic partnership model, the successful integration of recent acquisitions in France and Italy and exceptional items linked in particular to revaluation of equity investments.

Gross written premiums for the BNP Paribas Group’s Insurance Business Line reached 40.5 billion euros, an increase of 12% compared to 2024. BNP Paribas Cardif’s business is driven by dynamic performance across the BNP Paribas Group’s Retail Banking network and by a unique partnership model that enables it to generate 54% of its gross written premiums with partners and networks outside the BNP Paribas Group. Nearly

80 partnerships were renewed or signed in 2025, testifying to the confidence partners have in BNP Paribas Cardif’s capacity to support the goals of their customers. These new agreements include a partnership in France with Stellantis Financial Services in the used car business, consolidating the leading position of Icare, BNP Paribas Cardif subsidiary specialized in extended warranties and maintenance for motor vehicles.

Deployed in 30 countries this model enabled BNP Paribas Cardif to generate 52% of its gross written premiums outside of France in 2025, consolidating growth thanks to new strategic alliances.

Continued growth in savings

Savings assets under management totalled 302 billion euros at the end of 2025 (+6% compared to end 2024). Gross inflows in savings worldwide amounted to 32.4 billion euros at the end of 2025, (+15% compared to end 2024), with 37% in unit-linked products. In France, savings inflows increased 3% comported to 2024, reaching 17.4 billion euros. This increase came in particular from retail banking networks of the BNP Paribas Group, as well as business through wealth management advisors and brokers, and from the integration of Neuflize Vie. Outside France, gross savings inflows were 14.9 billion euros, an increase of 32% over 2024. The acquisitions of Neuflize Vie and BCC Vita enabled BNP Paribas Cardif to consolidate its leadership in savings by taking advantage of new distribution channels.

BNP Paribas Cardif, a major player in life insurance vehicles in France, and maintains the remuneration rate for its life insurance and capitalisation contracts in 2025 with an average rate of 2.92%. Thanks to substantial reserves and diversified allocation of assets, the insurer confirmed the solidity of its euro fund. Once again, this year, reflecting an equitable approach and supported by a unified rate policy, clients will benefit from a net rate1 excluding bonuses of at least 2,75%2 for 97% of its contracts3, regardless of when the product was subscribed and the distribution channel. BNP Paribas Cardif also strengthened its partnership with BNP Paribas Asset Management, the European leader in long-term asset management, delegating management of a portion of its general fund in France.

BNP Paribas Cardif has pursued its responsible investment policy, targeting both financial performance and positive impact on society in the management of savings entrusted to it by policyholders. At the end of 2025, 97% of the assets in the euro fund in France had undergone ESG4 analysis, and BNP Paribas Cardif had made 2.2 billion euros in positive impact investments, corresponding to an average of 2.1 billion euros per year since 2019. At 31 December 2025 nearly 25% of unit-linked assets were invested in responsible investment vehicles5. To support the transition to a low-carbon economy,

BNP Paribas Cardif has been committed since 2021 to reducing greenhouse gas emissions in its investment portfolios and to contributing to compliance with the Paris Agreement. The insurer strengthened its commitment in 2025, setting a target of reducing the carbon footprint6 of its directly held equity and corporate bond portfolio by 50% by 2030 (baseline 2020).

Strong positions in protection to make insurance more accessible

Protection gross written premiums reached 8.1 billion euros in 2025, an increase of 3% compared to 2024. Gross written premiums increased 3% in France to 2 billion euros at end 2025. Gross written premiums in international markets totalled 6.1 billion euros in 2025, an increase of 3% compared to 2024. In Latin America, gross written premiums were 1.8 billion euros, an increase of 3% compared to 2024. Gross written premiums in Asia totalled 1 billion euros, up 1% compared to 2024. In Europe (excluding France) and other countries, business posted a rise of 4% compared to 2024, reaching gross written premiums of 3.3 billion euros.

BNP Paribas Cardif is keenly aware of the importance of establishing relationships with partners and clients anchored in long-term confidence and has reaffirmed its commitment to make insurance more accessible. Faithful to this mission, the company works to ensure better insurance cover for its policyholders to protect them against unexpected life events while helping them realise their goals. By taking into account scientific and medical advances, the insurer continually adjusts its offers and subscription terms and has for more than 15 years regularly introduced concrete measures to facilitate access to creditor insurance. This approach expanded further in 2025 in France to include breast, prostate and testicular cancer survivors, who can now subscribe mortgage insurance without any additional premiums or exclusions, even before the legal period of five years established by the “right to be forgotten”.

Furthermore, BNP Paribas Personal Finance and BNP Paribas Cardif have introduced changes to creditor insurance linked to revolving credit offers available from BNP Paribas Personal Finance’s Cetelem brand, providing extended protection and more inclusive eligibility. Designed to address priorities expressed by people in France today, the policies offer broader, innovative coverage to reflect changes in society and demand for protection solutions. They include coverage of spouses without any additional fee, extended job loss coverage, new guarantees covering divorce or dissolution of civil partnerships, or family assistance if someone is obliged to stop working to care for a sick or disabled child or a dependent family member.

Technology and artificial intelligence help improve the customer experience

BNP Paribas Cardif has for many years introduced initiatives to improve the customer experience thanks to technology, while maintaining the highest standards to meet the growing expectations of its clientele. BNP Paribas Cardif remains more convinced than ever that the human dimension remains an essential pillar in the customer relationship. Recognizing the potential of artificial intelligence (AI), BNP Paribas Cardif deploys an international network of 140 experts who focus their efforts on developing and deploying innovative and secure solutions for the insurer’s partners, policyholders and employees.

By embedding technology and AI in the claims management procedure, for example,

BNP Paribas Cardif boosts the efficiency of claims processing. In France, the insurer has worked with Orange to introduce a solution for AI-based automated claims approval for 50% of claims involving breakage or oxidation of mobile devices. Another example is optimisation of the process for claims under the personal protection product “Solution Prévoyance” marketed via the BNP Paribas retail banking network in France. A digital platform available via mobile phone or the web has been rolled out and has cut claims processing time by 3/4. In Brazil, the claims management model combines digital efficiency and human support: 96% of claims are reported digitally and 90% are settled on the same day. Unemployment claims have recorded strong customer satisfaction, with a Net Promoter Score (NPSD) of 75.

BNP Paribas Cardif also introduces innovative solutions upstream from sales to deliver greater value to its customers. Developed for BNP Paribas Cardif’s partner Falabella – a major retailer in Chile – the CarBoosting tool uses AI to enable dynamic pricing for car insurance. This solution enables real-time review and adjustment of premiums to guarantee personalised rates for each customer.

1Net of management fees before French social charges

2Plus entry bonuses

3For Cardif Assurance Vie entity

4Environmental, Social and Governance criteria

5A unit-linked asset is considered “responsible” if it has received a label from an independent organisation (for example SRI, GreenFin, FNG, Finansol, LuxFlag ESG, Towards Sustainability) or classified as Article 9 under the European Union’s Sustainable Finance Disclosure Regulation (SFDR).

6Carbon footprint in scope 1 and 2, excluding unit-linked funds. Objective dates: 12/31/2020 – 12/31/2029.

Emmanuel Gendreau has been appointed Director of BNP Paribas Epargne & Retraite Entreprises, effective from 5 January 2026. He succeeds Nicolas Villet, who has been appointed Director of the EMEA (Europe, Middle East, Africa) region at BNP Paribas Cardif. Emmanuel Gendreau joins the executive committee of BNP Paribas Cardif France and will report to Charlotte Chevalier, Deputy Chief Executive Officer of BNP Paribas Cardif Head of France and Luxembourg.

BNP Paribas Epargne & Retraite Entreprises is the entity specialising in corporate savings solutions (employee savings and collective retirement savings), co-managed by

BNP Paribas Asset Management for financial management, and BNP Paribas Cardif for insurance activities. At the end of 2024, the company managed

€30.2 billion in assets for 26,000 businesses and for 1.6 million savers.

Emmanuel Gendreau joined the

BNP Paribas Group in 1998. After holding various positions, notably in mergers and acquisitions within BNP Paribas Group Financial Management department, he became Managing Director at Financial Institutions Coverage at BNP Paribas CIB in 2005. He covered major French insurers as a Senior Banker and was appointed Global Head of Insurance in 2015. In 2021, he joined the Investment & Protection Services (IPS) division, responsible for Institutional Partnerships and the restructuring project of the division’s private assets activities. Following this restructuring, he was appointed Head of IPS Investments in 2023.

Emmanuel holds a master’s degree in management from ESCP Europe and a

Master 1 in Applied Mathematics from Université Paris IX Dauphine.

Read more

- Charlotte Chevalier has been appointed Deputy Chief Executive Officer, Head of France and Luxembourg,

- Maxime Boyer Chammard has been appointed Chief Operating Officer (COO), Head of Efficiency, Technology & Operations,

- Michael Nguyen has been appointed Chief Executive Officer of Asia,

- Nicolas Villet has been appointed Chief Executive Officer of EMEA (Europe, Middle East, Africa).

Charlotte Chevalier began her career at the Inspection Générale des Finances (IGF). From 2009 to 2016, she held several positions within the French Ministry of Finance (Tax Legislation Department and at the DGFIP) but also at the French Prime Minister Private office as an advisor in charge of tax policies. From 2016 to 2019, she was Director of Strategy and Transformation at Covea where she implemented digital transformation and competitiveness programs. In 2019, she joined the Transformation and Development Department of BNP Paribas Cardif as Head of Strategy and M&A, and Secretary to the Executive Committee of BNP Paribas Cardif. She then was appointed Chief Proposition Officer in 2021 and Chief Executive Officer of EMEA (Europe, Middle-East, Africa) in 2023.

Charlotte Chevalier is a graduate of Sciences-Po Paris, ENSAE and the National School of Administration.

Maxime Boyer Chammard began his career with the

BNP Paribas Group in 2000, where he held several management positions in France. In 2010, he was appointed Chief Operating Officer (COO) of

BNP Paribas Financial Services in the United States, then Chief Operating Officer (COO) of BNP Paribas Securities Services in the United Kingdom in 2013. His responsibilities include overseeing outsourcing services as well as implementing technology and business transformations. He was previously Global Head of Investment and Funds Services Operations at

BNP Paribas Securities Services, in charge of fund administration, transfer agency, middle office outsourcing, investment analytics and data services. Maxime Boyer Chammard was also a member of

BNP Paribas Securities Services Management Board and played a key role in client transformation initiatives, operational strategy and digital innovation.

Maxime Boyer Chammard holds a Master degree in management with a major in finance from ESSCA Business School.

Michael Nguyen started his career in Corporate Strategy and M&A in 2002 for the Airbus Group. From 2005 to 2016, he held various management positions for large global groups, including Bouygues and AXA. He joined the SCOR Group in 2016 where he was Group Head of Operations Strategy and Transformation. Directly reporting to the Group Chief Operating Officer (COO), he led SCOR’s operations strategy from planning to execution and oversaw the reinsurer’s strategic projects portfolio. Michael Nguyen joined BNP Paribas Cardif in 2020 as Chief Information Officer. He was then appointed Deputy Chief Executive Officer and Chief Operating Officer (COO) in charge of the Efficiency, Technology and Operations department of

BNP Paribas Cardif.

Michael Nguyen holds a Master of Science from Pierre and Marie Curie Paris University, a Master in management from HEC and Mines ParisTech, and a MBA from INSEAD.

Nicolas Villet began his career at Deloitte in the Financial Transactions and Valuations department. In 2009, he joined the Development department of the Casino Group, where he participated in the creation and development of GreenYellow. In 2011, he joined the

BNP Paribas Group to work in Finance management, then BNP Paribas Cardif in 2013 as Head of Strategy and Secretary of the Executive Committee. In 2016, he continued his career in Hong Kong as Chief Financial Officer and then as Deputy Chief Executive Officer

of BNP Paribas Cardif in Asia. In 2020, he was appointed Head of BNP Paribas Epargne & Retraite Entreprises and Deputy Chief Executive Officer of

BNP Paribas Cardif France in 2024.

Nicolas Villet is a civil engineer from the Ecole des Mines and a graduate of HEC Paris.

Photos are available from the BNP Paribas Cardif press office.

Read more

The insurer BNP Paribas Cardif has purchased an office building located at 8 place de la Bourse and 5-9 rue Feydeau in Paris from a French institutional investor.

The property encompasses two buildings built between 1920 and 1951 to house a telecommunications centre. It has eight floors and approximately 6,500 square metres of floor space. Given the unique architectural features of the building on Place de la Bourse, it is listed as a heritage asset.

The building was completely renovated in 2021 and contains office spaces of between 500 and 800 square metres. In addition, an underground level has parking space for 19 cars, 24 motorcycles, plus a bicycle parking area. It also has approximately 500 square metres of accessible exterior space and is fully leased to several different businesses.

This acquisition enables BNP Paribas Cardif to pursue its investment strategy and diversify assets for its policyholders. The transaction was carried out via the Cardimmo unit-linked real estate investment vehicle managed by BNP Paribas Cardif, and via its pension savings euro fund.

BNP Paribas Cardif was advised by Wargny Katz, Jadero, Opéra Avocats, David Colin (attorney) and Ikory Project Services.

Read more

More than four out of five financial advisors (85%) express confidence in their business for the coming 12-month horizon.

- 67% of financial advisors report a year-on-year increase in the number of clients.

- 78% of financial advisors believe their clients are concerned about their investments given the geopolitical and economic situation.

- 58% of financial advisors believe their clients will track the performance of their asset allocations more closely, 57% the diversification and 54% the level of risk over the coming 12 months.

- A third of financial advisors (34%) say they plan to offer more individual pension products.

- A quarter of financial advisors (27%) now regularly employ artificial intelligence (AI) in their work.

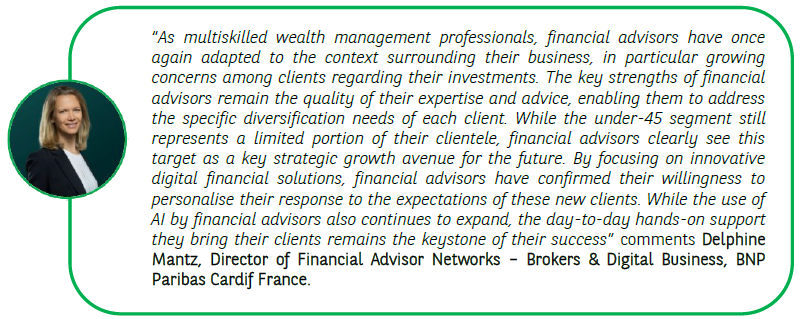

BNP Paribas Cardif has released the results of its 19th annual survey of financial advisors. Conducted with Kantar, one of the world’s leading market research agencies, the 2025 survey confirms that financial advisors play a central role in defining investment strategies, with a focus on product diversification and by proposing a range of thematic investment options.

Dynamic, attractive, confident: the profession stays the course in a changing world

The current environment introduces new challenges. A full 78% of financial advisors believe their clients are concerned regarding their investments given evolving geopolitical and economic factors – up 25% since 2024 and a record figure, even compared with levels of concern measured when the Covid pandemic ended. The international geopolitical climate is the primary negative factor impacting business activities, say the financial advisors (72%), 18% more than last year. This is followed by regulatory factors (retail investment strategy requirements were cited by 48% of respondents, and the “Green Industry Law” by 45%), alongside the economic context (47%). At the same time, financial advisors listed AI and the profit-sharing law as elements that create opportunities (54%) and could drive business growth.

Nevertheless, this finding contrasts with the positive mindset among financial advisors and the development of the profession. More than four out of five (85%) financial advisors expressed confidence in the coming 12 months, reflecting the dynamic outlook for the profession, thanks in particular to the growth of their clientele franchise: 67% of financial advisors reported an increase in clients compared with the previous year. Despite economic and geopolitical turbulence, the profession is doing well. Both the confidence of the financial advisors themselves and the confidence their clients have in their expertise continue to rise.

The three fundamentals for financial advisors remain performance, risk management and diversification

Financial advisors believe that economic uncertainties have led clients to seek safer investments (63%) and diversification, both within and outside the framework of life insurance investment vehicles (52%). They believe these expectations will be confirmed in coming months, and over half of them think their clients will want greater diversification, both in their portfolios (57%) and in terms of risk exposure (54%). In line with results from the previous three surveys, however, performance remains a top-of-mind factor, since 58% of financial advisors say their clients will be looking more closely at yield.

This demand for diversification is reflected in the wealth management products and solutions offered by financial advisors within the scope of life insurance vehicles and capitalisation contracts. While 61% of financial advisors plan to take advantage of opportunities related to investments in French and European defence and sovereignty, 56% intend to propose thematic funds (innovation, tech, health, energy, etc.). In addition, financial advisors plan to propose more ETFs (43%), private equity investments (37%), structured products (35%) or discretionary portfolio management products (28% of respondents this year, compared with just 13% in 2024).

In addition to life insurance vehicles, financial advisors have a clear and focused strategy and are addressing current social and economic issues regarding pension planning. Some 59% of financial advisors plan to promote pension savings solutions (34% individual and 25% collective). Half the financial advisors also plan to target protection insurance in their business portfolio within the next two years (29% individual protection and 21% collective protection).

Financial advisors seek to diversify client franchise and target younger population segments

As proven experts in wealth management, financial advisors are well-positioned to adapt to the variety of needs and expectations of their clients. Their top challenge today is to renew and diversify the makeup of their clientele franchise, adding younger profiles in particular (under 45). This segment is seen as a strategic avenue for growth by 90% of the respondents. Nearly half the financial advisors (49%) report that their client base is already becoming younger.

This new younger clientele segment is dynamic and actively engaged, with new habits and behaviours. Some 83% of financial advisors note their independence and high level of digital adoption, 42% say these clients have a higher appetite for risk, and a third (33%) note that they are more financially savvy. Demonstrating their ability to adapt to market shifts and align with these profiles, 42% of financial advisors focus on structured products for this clientele, 34% on ETFs and 26% on private equity.

A third of the financial advisors (31%) now count new socio-professional profiles in their clientele.

Strategic use of AI accompanied by monitoring of regulatory compliance figures among top priorities for financial advisors

Fast-paced changes require financial advisors to continually adapt and learn. For 71% of survey respondents, the primary challenge is ensuring regulatory compliance, ahead of adopting AI (44%) or changing investment solutions to adapt to the economic climate (38%). What’s more, half the financial advisors (52%) say they would be interested first and foremost in training centred on regulatory developments.

Lastly, 54% of financial advisors believe artificial intelligence will have a positive impact on their business, an increase of 14% over last year. A full 56% of financial advisors already use AI – regularly or occasionally – to automate or facilitate certain tasks, up from only 23% in 2024. On the other hand, the use of AI will remain primarily concentrated on automation of repetitive administrative tasks (79%), as well as for monitoring regulatory and compliance issues (67%).

Nearly a third of financial advisors (28%) believe their clients feel that personal contact will remain the cornerstone of the relationship with their advisor, and 64% say that AI will not have any direct impact on their client relationships. The expertise of financial advisors and personal support remain key to the added-value delivered by financial advisors and constitute the very heart of the profession.

BNP Paribas Cardif has finalised the acquisition of AXA Investment Managers (AXA IM) and signed a long-term partnership with the AXA Group to manage a large part of its assets.

This operation, announced on 1st August 2024, will enable the BNP Paribas Group to create a leading European asset management platform with over EUR 1.5 trillion in assets under management entrusted by its clients. It allows the Group to become the European leader in long-term savings management for insurers and pension funds with around EUR 850 billion, with the ambition to become the European leader in fund collection for private asset investments and positioning itself among the main providers of ETFs in Europe. This operation is also part of the Group’s core mission to support the economy by mobilising savings to finance future-oriented projects in the best interests of its clients.

By combining the expertise of AXA IM, BNP Paribas Asset Management, and BNP Paribas REIM, this new platform will have a wide range of traditional and alternative assets, an expanded global distribution network, enhanced innovation capabilities, and a more comprehensive offering in responsible investment. It will benefit from AXA IM Alts’ market position and expertise in private assets, which are key drivers of future growth for institutional and individual clients, as well as AXA IM’s know-how in long- term asset management for insurance and retirement. In this context, BNP Paribas Cardif will leverage the capabilities of this platform for the management of a large part of its assets, notably its general funds.

The formation of this new platform marks a major milestone in the development and growth journey of the IPS division. It will fully benefit from BNP Paribas’ integrated model, in close collaboration with the CPBS and CIB businesses, particularly within the framework of the “originate to distribute” approach.

“This acquisition is an important moment for the entire BNP Paribas Group. We are delighted to welcome the AXA IM teams, who will find within the BNP Paribas Group a strong culture of customer service as well as ambitious growth and innovation prospects. These are teams with recognised and complementary expertise that will build together a European industrial project to better serve our clients. I have every confidence in the ability of the management teams of our asset management activities to grow the business and create value for our clients and employees,” said Jean-Laurent Bonnafé, Director and Chief Executive Officer of BNP Paribas.

Joint working groups with AXA IM teams are already in place to reflect on and develop a common roadmap, particularly with regard to offerings and services. This roadmap will be submitted to the appropriate employee representative bodies.

The project to merge the legal entities of AXA IM, BNP Paribas AM and BNP Paribas REIM, which would create the new platform held by BNP Paribas Cardif, is currently the subject of consultation with employee representative bodies.

Sandro Pierri, CEO of BNP Paribas AM, will lead the BNP Paribas Group’s asset management activities and Marco Morelli, the current Executive Chairman of AXA IM, will chair the BNP Paribas Group’s asset management activities.

From a financial perspective:

- The Group’s revenue growth by 2026, including the impact of the transaction, will be greater than +5% (CAGR 24-26), with an average annual jaws effect of +1.5 pts.

- Return on Invested Capital (ROIC) will be more than 14% in year three (2028) and more than 20% in year four (2029).

- From a prudential perspective, the impact of the operation on the Group’s CET1 ratio is estimated at approximately -35bp as of the 3rd quarter 2025 results, discussions with supervisory authorities are still on going.

An update on the progress of the operation will be provided upon the release of the third-quarter 2025 results ahead of a Deep Dive, that will take place during the first quarter 2026, focused on the Group’s trajectory including this operation.

- Pre-tax net profit of 1.6 billion euros for full-year 2024, up 13% compared to 2023

- Gross written premiums of 36.4 billion euros at end-2024, up 21% compared to 2023

- 287 billion euros in assets under management, up 13% compared to 2023

- Over one hundred partnerships renewed or signed in 2024

“2024 was a very good year for BNP Paribas Cardif, with record revenues and a sharp rise in pre-tax net profit. Our business is dynamic and is based on strong savings inflows and robust partnerships. Our diversified partnership model has once again demonstrated its effectiveness and allows us to consolidate our leading positions in savings and protection. Making insurance more accessible guides us on a daily basis and over the long term. Through this commitment, we are firmly focused on supporting our policyholders’ projects, providing insurance coverage for as many people as possible. Finally, in a continuous improvement approach, we accelerate thanks to artificial intelligence and the implementation of new technologies, in a secure way and a strengthened customer experience.” commented Pauline Leclerc-Glorieux, Chief Executive Officer of BNP Paribas Cardif.

2024 results up sharply

BNP Paribas Cardif continued its growth trajectory with pre-tax net profit of 1.6 billion euros in 2024, up 13% compared to 2023. Gross written premiums for the BNP Paribas Group’s Insurance Business Line reached 36.4 billion euros, an increase of 21% compared to 2023. At the end of 2024, assets under management totalled 287 billion euros, up 13% compared to the end of 2023.

BNP Paribas Cardif operates in 30 countries and generates nearly half of its gross written premiums (48% in 2024) outside of France. Leveraging its diversified partnership model, the insurer, a global leader in bancassurance partnerships, generates more than half of its gross written premiums (52% in 2024) with partners outside the BNP Paribas Group.

Gross inflows in savings worldwide amounted to 28.3 billion euros at the end of 2024 (+24%), with 34% in unit-linked products. In France, savings inflows increased by 15% compared to 2023, reaching 16.9 billion euros. Internationally, gross inflows stood at 11.5 billion euros, up 40% compared to 2023.

Protection gross written premiums reached 8 billion euros in 2024, up 11% compared to 2023. In France, gross written premiums were up 5% to 1.9 billion euros, energised by property and casualty insurance, which recorded 12% growth, and by affinity insurance with nearly 1.9 million customers at the end of 2024. In international markets, protection gross written premiums reached 6.1 billion euros, an increase of 14% compared to 2023. Growth in Latin America was driven by the rollout of long-term partnerships, particularly in Brazil, where gross written premiums totalled 1.9 billion euros, up 13% compared to 2023. In Europe (excluding France) and other countries, business was up 16% over 2023, with gross written premiums of 3.2 billion euros. Asia recorded gross written premiums of 1.1 billion euros (+10% compared to 2023).

Over one hundred partnerships renewed or signed in 2024 to strengthen products and services for policyholders

The strength of BNP Paribas Cardif’s partnership model was once again manifest in 2024 with the development of key partnerships in Italy with the BCC Iccrea cooperative banking group and in France with the private bank Neuflize OBC. These two major partnerships will enable the insurer to consolidate its leadership in savings and tap into new distribution networks. In France, BNP Paribas Cardif, convinced that life insurance is an essential vehicle that allows French savers to grow their savings and at the same time help finance the economy, relies on a diversified euro fund with a net rate excluding bonuses of at least 2.75% for 96% of its life insurance and capitalisation contracts in 2024. A prudent long-term management strategy and solid reserves allow BNP Paribas Cardif to support its policyholders’ projects and savings objectives over extended periods, with attractive returns on their savings.

The renewal or signing of over one hundred partnerships in 2024 will support long-term business development and strengthen product offerings for policyholders. This dynamism is reflected in new agreements in creditor insurance, a segment where BNP Paribas Cardif is the global leader*. In France, for example, BNP Paribas Cardif has concluded a new partnership with Simulassur, the Magnolia Group’s B2B marketplace specialising in loan insurance, to expand access to its “Cardif Libertés Emprunteur” contract to new brokers and clients. It has also launched new creditor insurance offerings, including in the Nordic countries with the digital bank Northmill. At the beginning of 2025 in France, BNP Paribas Cardif continued to develop its affinity insurance business, notably with the renewal of its partnership with Orange.

Positive impact drives growth and trust for clients and partners

As shown by the results of the global study entitled “Protect & Project Oneself” , conducted by BNP Paribas Cardif, demand for protection insurance remained significant in 2024. To address concerns and support individual client projects, BNP Paribas Cardif is continually guided by its mission to make insurance more accessible. By making insurance more inclusive, more understandable, easier to subscribe and to use, BNP Paribas Cardif helps individuals better protect themselves to better plan for the future. This is the case in individual protection solutions with the introduction of a new and educational approach based on a personalised diagnosis, allowing BNP Paribas French Commercial Banking to offer clients the most appropriate level of protection for themselves and their loved ones. This approach as a responsible insurer is also reflected in improving subscription conditions for creditor insurance for people undergoing treatment for HIV in France, going beyond the criteria set by the AERAS agreement, by now approving without additional premium surcharge or exclusions patients with an undetectable viral load at the time of subscription and for loans up to €1 million. This action is part of a broader approach taken for over the past 15 years to offer coverage to the most vulnerable segments of the population under optimal terms and conditions. Additionally, in 2024, BNP Paribas Cardif expanded coverage of the Total Temporary Disability guarantee in its “Cardif Libertés Emprunteur” contract, marketed in France by brokers, financial advisors, and on Cardif.fr. This “Family Assistance” guarantee – which has two components, “parental presence” and “family caregiver” – now better meets the expectations of families facing difficult life events.

BNP Paribas Cardif considers positive impact to be a foundational element in its investment strategy, convinced that this commitment is a factor that nurtures trust among its clients and partners. The insurer implements a responsible investment policy and applies an ESG filter to investments in its general fund. In 2024, 96% of the assets in BNP Paribas Cardif’s euro funds in France underwent ESG analysis, and more than 33% of unit-linked assets are invested in responsible vehicles , representing 19.4 billion euros. BNP Paribas Cardif, which actively implements the BNP Paribas Group’s energy transition policy, has been committed since 2021 to supporting the transition to a low-carbon economy reducing greenhouse gas emissions in its investment portfolios and contributing to compliance with the Paris Agreement. At the end of 2024, the carbon footprint (Scopes 1 and 2 ) of its directly held equity and corporate bond portfolio in the assets of its euro funds had continued to decrease by at least 50% compared to the end of 2020. This approach is also supported by investments aimed at supporting impact initiatives. BNP Paribas Cardif recorded 3 billion euros in positive impact investments addressing environmental and societal issues during 2024, which corresponds to an average of 2 billion euros per year since 2019.

This commitment to positive impact for the benefit of stakeholders is also reflected in actions taken by BNP Paribas Cardif in favour of a more inclusive society. In 2024, BNP Paribas Cardif and Sistech, an association that supports employment for refugee women in technology and digital professions, signed a partnership to support the association’s beneficiaries. The initiative is part of the “Women & Girls in Tech” program, supported by the BNP Paribas Group. This program aims to promote the recruitment of women in digital and IT fields. In addition, because the number of obesity cases is increasing significantly worldwide, BNP Paribas Cardif has been mobilised since 2021 around the prevention of overweight and obesity. The approach centres on funding research with an international group of doctors and nutrition expert researchers, and supporting several associations worldwide dedicated to preventing overweight and obesity in young people. The program has already benefited 650,000 children and 2 million people, including their family members, in 13 countries.

Technology and artificial intelligence to better serve human needs and increase customer satisfaction

BNP Paribas Cardif firmly believes that technology, particularly artificial intelligence, is key to improving customer satisfaction and supporting partners with quality products and optimised processes. Some 80 AI use cases are currently in production at BNP Paribas Cardif, including 20 dedicated to claims management. The “CardX” solution developed in 2021 to accelerate claims management and automate document processing already handles over 50,000 pages per month in Brazil, Colombia, Spain, and Poland in 2024. New solutions were also deployed in 2024, including with Orange in France, where BNP Paribas Cardif introduced an automatic claims acceptance process based on a score calculated using artificial intelligence. This allows eligible claims declared by policyholders for their mobile devices to be accepted in just seconds.

An insurer’s business involves numerous interactions with its clients. For BNP Paribas Cardif, analyzing and understanding this mass of information is essential to meet the needs for immediacy and efficiency. Its objective is to design simple and accessible customer experiences to meet its three major challenges: raising the level of protection for a greater number of policyholders through greater personalisation and loyalty, improving the customer experience through automation, and optimising processes to meet the expectations of customers and partners.