In this new opinion piece, Nathalie Doré, Chief Impact & Innovation Officer shares her insights on the role of insurer in addressing growing social vulnerabilities.

As vulnerabilities increase in a world facing multiple, overlapping crises, insurers are doing far more than simply covering claims. They play a vital role in supporting society as a whole, particularly through prevention and inclusion initiatives. This role will become increasingly important in light of the societal challenges expected over the next decade, especially in the social sphere: ageing populations, the rise of solo living, emerging human and animal diseases, disinformation and more...

Corporate social responsibility at the heart of insurance risk pooling

In recent years, corporate social responsibility (CSR) has focused on two major areas:

- incorporating environmental social and governance (ESG) criteria into corporate decision-making

- Increasing the positive impact of business activities

In insurance, this concept of impact is embedded in our DNA through the principle of risk pooling.

One of the key benefits of risk pooling is accessibility. Without it, the coverage offered by insurance companies would generally be less affordable. By pooling risks, all policyholders share the costs, making insurance coverage more accessible to the most vulnerable members of society.

Prevention: an additional safeguard against social risks

Today, we are frequently warned about the rise in environmental risks and are seeing insurers introduce numerous prevention plans and rightly so. However, it is equally crucial to address social risks, as these are also increasing and can have a lasting impact on individuals and communities. Environmental and social risks are, moreover, often interconnected.

Through their prevention programmes, insurers can play an important role. Take obesity, for example a complex chronic disease that has reached pandemic proportions worldwide. Despite this alarming situation, the World Health Organization maintains that the trend can still be reversed. An analysis of the WHO Acceleration Plan to Stop Obesity shows that prevention measures account for a significant part of the solution.

Such initiatives already exist and have demonstrated their effectiveness, particularly among children, as childhood is when lifestyle habits are formed and when the combined influence of schools and families is especially strong.

Data from trials to which we have contributed show that multi-component school-based interventions combining physical activity, nutrition, health education and parental involvement are particularly effective in preventing excess weight among children in this age group.

Including the most vulnerable by understanding the

different forms of vulnerability

Inclusive involves making insurance products and services designed for people in vulnerable situations accessible thought:

- Affordable pricing

- Specific coverage

- Innovative distribution channels

With the aim of providing them with effective protection.

According to the world health organization, an individual’s’ vulnerability is shaped by physical, social, and environmental factors or process that increase their susceptibility to the impact risks. Three main forms of vulnerability are generally identified

- Health-related

- Social

- Economic vulnerability

For vulnerable populations, access to prevention programmes can provides an additional layer protection. The challenge lies in reaching the most vulnerable.

The insurer’s role is to maximise inclusivity in a complex environment by offering policies that enable people to pursue their life goals. This requires greater access to data, together with its responsible use, in order to avoid excessive personnalisation where this could undermine risk pooling

In the recent years, the insurance industry has made significant progress in developing more inclusive products, particularly in the field of creditor protection insurance. People with aggravated health risks including inflammatory bowel disease, HIV and certain cancers can now obtain coverage that was previously denied or severely restricted.

This progress has been made possible by advances in medicine and across the healthcare

ecosystem as a whole. A better understanding of medical conditions, how they develop and how they are treated enables insurers to refine their risk assessments and expand the scope of insurability.

The AERAS Convention (France) has, of course, played a leading role in extending access to insurance for these groups. But progress does not stop there: several insurers, including BNP Paribas Cardif, are now going beyond the required thresholds, driven by a positive approach designed to serve policyholders’ interests.

In an intermediated distribution model, this goal of inclusion is pursued together with insurance distribution partners. It involves incorporating coverage and services that make protection more effective for end customers while also improving distribution efficiency by limiting refusals and premium surcharges.

Additional mechanisms, such as social action funds, can also provide exceptional support to the most vulnerable populations. If every stakeholder contributes, initiatives that may appear modest at the level of a single company can collectively have a positive impact on society.

Increasing the transparency of insurance offerings

Social inclusion is a central issue because it determines people’s ability to pursue their life goals and contributes to economic and social stability in an uncertain and volatile macroeconomic environment.

Nathalie Doré, Chief Impact & Innovation Officer

Understanding societal challenges and modelling the new risks associated with them enables insurers to ask the right questions: do we currently have the right products to address these risks? If not, how can we adapt them for example, for people experiencing financial vulnerability or facing aggravated health risks?

Maximising insurance’s social impact also requires clear and accessible communication with policyholders. Studies show that there is a strong need for greater education and transparency regarding coverage and policy terms. New online assistants can help people understand insurance products and coverage, provided that they are:

- Free from bias

- Deliver accurate answers

- Handle the data they use appropriately.

Driving progress across the entire market

Continuing to move the market forward requires action across several complementary areas:

- Making insurance offerings easier to understand.

- Strengthening prevention

- Establishing shared industry definitions and standards.

This progress can also be supported by greater market-wide transparency for example, through more systematic reporting of acceptance rates to make improvements visible and encourage increasingly inclusive practices.

By expanding coverage and making protection more effective, the insurance industry will

strengthen its social role over the long term.

READ MORE

Mumbai, July 24th, 2026 – BNP Paribas Cardif, the insurer of BNP Paribas Group, has entered into a definitive agreement to acquire a ~26% stake in IndiaFirst Life Insurance Company Limited (IndiaFirst Life) from Warburg Pincus. The transaction is subject to regulatory approvals.

The transaction marks a significant milestone in IndiaFirst Life’s growth journey and reinforces the long-term commitment of its shareholders to supporting the company’s growth in the Indian life insurance market.

Upon completion of the transaction, IndiaFirst Life’s shareholding will comprise Bank of Baroda (~65%), BNP Paribas Cardif (~26%) and Union Bank of India (~9%).

By combining Bank of Baroda’s strong branch network, IndiaFirst Life’s multi-channel distribution strength and BNP Paribas Cardif’s global bancassurance expertise, product innovation and insurance capabilities, the shareholders aim to accelerate IndiaFirst Life’s next phase of growth. The partnership reinforces the company’s ambition to become India’s preferred life insurance partner.

For BNP Paribas Cardif, the transaction marks a further step in its international growth and diversification strategy, while strengthening its presence in Asia, particularly in India, a strategic market offering compelling long term growth opportunities. It reinforces BNP Paribas Cardif’s partnership-led business model and strengthens its position in a dynamic insurance market.

Pauline Leclerc-Glorieux, CEO, BNP Paribas Cardif said

“We are very pleased to announce this new partnership with Bank of Baroda, a major bank in India, a key strategic market with a compelling growth opportunity for BNP Paribas Cardif. This transaction will further drive our international growth strategy of partnering with strong institutions in high-potential markets. We will leverage our global bancassurance and partnership expertise to support the next phase of development of IndiaFirst Life in India, with a focus on enhancing the accessibility of insurance products for the Indian population.“

Dr. Debadatta Chand, Chairman, IndiaFirst Life and MD & CEO, Bank of Baroda, said “This transaction represents a meaningful step in IndiaFirst Life’s long‑term strategic journey and reflects the reinforced commitment of its shareholders to the company’s continued growth. With BNP Paribas Cardif joining us as a partner, we are extending a relationship that has already proven successful through our joint venture in asset management, and we look forward to leveraging their global insurance expertise alongside Bank of Baroda’s extensive distribution franchise and deep local market insights. Together, we remain focused on broadening access to quality protection and savings solutions for customers across India.”

Sanjay Singh, CEO and Head of Territory,

BNP Paribas in India, said “India is a strategic market for BNP Paribas Group, and this transaction reinforces our long-term commitment to delivering global expertise and creating sustainable long-term value. Building on our longstanding relationship with Bank of Baroda, this investment brings together complementary strengths, combining BNP Paribas Cardif’s global insurance capabilities with deep local market knowledge. Together, we are well positioned to support the continued development of India’s insurance ecosystem.”

Narendra Ostawal, Managing Director and Head of India Private Equity, Warburg Pincus, said

“IndiaFirst Life has demonstrated resilience, disciplined execution, and a strong customer-centric ethos throughout its journey. We are proud to have partnered with the company during an important phase of its development and to have worked alongside management and our fellow shareholders to support its growth, strengthen its franchise and help position the business for long-term success. This transaction reflects the significant progress IndiaFirst Life has made over the course of our partnership. With BNP Paribas Cardif now joining as a strategic shareholder and bringing deep global insurance capabilities, IndiaFirst Life is well placed to accelerate its next phase of growth. We remain confident in the company’s long‑term trajectory and wish the company continued success.”

Rushabh Gandhi, Managing Director & CEO, IndiaFirst Life, said “We are delighted to welcome BNP Paribas Cardif as a new shareholder alongside Bank of Baroda. Their partnership, product innovation, and operations complement our distribution strengths and digital execution capabilities. This collaboration will help us scale our mission to deliver simple, trusted, and technology-enabled life insurance solutions at scale. It will also support sustainable and profitable growth, while keeping us firmly focused on delivering superior customer outcomes. We would also like to thank Warburg Pincus for its partnership over the years, which has been invaluable during an important phase of our journey.”

The Innovation Ambassadors program, which includes 5 winners among 102 innovative projects submitted from 24 entities worldwide in 2025, shows that innovation can be found everywhere at

BNP Paribas Cardif!

Briefly introduce yourself

I am part of the « Cross-Coordination » Service within «the Efficiency, Technology & Operations » Department in Luxembourg. On a daily basis, we support the management of Cardif Lux Vie in continuously improving the processing of operations by providing expertise, recommendations, and performance management.

We get involved in framing initiatives (pre-projects), change management, tracking performance indicators, and setting up dashboards. We also contribute to risk management and strengthening operational quality.

More specifically, my role in this automation project was to represent our business areas, identify pain points, and then co-design with the teams a completely rethought processing workflow, all the way to validating the key steps of the system.

Present your initiative

The “KYC AML Recertification Automation” project was born from a simple observation:

Our file volumes and regulatory requirements are increasing, while teams are still dedicating a significant portion of their time to repetitive tasks. The challenge was therefore to design a more efficient and scalable process, capable of absorbing this growth while ensuring a high level of quality.

To achieve this, a cross-functional team was formed, bringing together business units, Data, Analytics, IT, and Group stakeholders. On the Data/Analytics side, data scientists developed an AI model to accelerate file processing, fully compliant with the Group’s Analytics governance framework. Close collaboration with all stakeholders including our counterparts at BGL BNP Paribas in Luxembourg enabled us to integrate operational constraints and ensure a deployment perfectly aligned with on-the-ground needs.

How does your initiative correspond to the category won?

Standardizing the process and automating first-level checks that is, the verifications carried out before any in-depth analysis, like checking the validity of ID documents, the consistency of declared information, etc, helps to harmonize practices, limit manual interventions, and significantly reduce processing time.

This development has strengthened our ability to handle high volumes of files, while maintaining a quality level that meets regulatory requirements. Its distinctive feature lies in the combination of technological innovation (the first AI model for Cardif Lux Vie, a life insurance company.

among the major market players in Luxembourg, belonging to the BGL BNP Paribas Group) and risk management.

The AI model is used as a triage tool to guide the analysis towards files requiring an in-depth review, within a defined governance framework (validation rules, traceability).

What are the next steps for your initiative?

As part of our ongoing approach, we have identified two main areas:

- First, we’re going to roll out this solution on a larger scale, extending it to cover more complex types of products, especially for the periodic recertification of our contracts. The goal is to speed up review cycles, ensure compliance, and better handle peaks in activity.

- Next, we want to apply this approach to onboarding new clients. Specifically, this means further automating client acceptance and the processing of new operation requests, making the collection of information, document validation, and consistency checks smoother.

What are your tips for innovating at BNP Paribas Cardif?

You need to dare, test, learn, encourage the sharing of experiences, and above all, hairness the power of collective and intelligence

READ MORE

Our new video series, Inside the Action, shines a spotlight on key initiatives led by BNP Paribas Cardif employees in France and internationally

Since June 2024, BNP Paribas Cardif and BCC Vita have joined forces in Italy through a long-term partnership, combining international insurance expertise with the local cooperative banking network of the ICCREA Group. In this new edition of Inside the Action, Giulia Galbiati, Chief of Staff at BCC Vita, explains how this collaboration is already delivering tangible results while laying the groundwork for future growth.

A Winning Alliance for Italian Insurance This partnership is built on complementary strengths.

- BCC Vita enhances its offering through BNP Paribas Cardif’s international expertise

- BNP Paribas Cardif expands its presence in Italy via a trusted network of local banks, reaching more customers.

It’s a win-win collaboration: we combine local proximity with global innovation for more effective insurance.

Giulia Galbiati, Chief of Staff, BCC Vita

Concrete Results from the First Months Teams have quickly implemented operational improvements :

- Expanded product range to meet diverse customer needs.

- Simplified sales processes for smoother subscriptions.

- Strengthened customer support for an optimized experience.

A Long-Term Vision for Insurance in Italy Designed to last, this partnership evolves alongside BCC Vita’s strategic plan, aiming to :

- Develop innovative solutions tailored to the Italian market.

- Unlock the full potential of this unique collaboration.

- Support BNP Paribas Cardif’s growth in Italy while driving BCC Vita’s transformation.

With BNP Paribas Cardif, we are building a new dynamic for insurance in Italy, benefiting customers and banking partners alike.

Giulia Galbiati, Chief of Staff, BCC Vita

Read more

The 10th edition of VivaTech, Europe’s leading event dedicated to technology and start-ups, took place in Paris from 17-20 June, 2026.

For BNP Paribas Cardif, this new edition was the opportunity to connect with the global innovation ecosystem, with the ambition to explore and engage in discussions around the technologies that will shape the future of insurance and better meet our partners’ and their clients’ needs.

Over the course of these four days, our guests (partners and collaborators) had the opportunity to engage with entrepreneurs, decision-makers and experts on today’s key technological challenges, such as artificial intelligence, cybersecurity, healthcare and digital sovereignty.

What to take away from BNP Paribas Cardif’s presence at Vivatech ? 🚀

BNP Paribas Cardif led two keynote sessions which allowed the insurer to showcase its expertise in artificial intelligence and power to transform insurance and banking services.

An AI at the service of financial advice

The 17th June : Delphine Mantz Director of Financial Advisors Networks – Brokers at BNP Paribas Cardif France and Marc Rousseau , co-founder of Ploovers shared a common vision: using artificial intelligence to enhance financial advice and makes it personalised, transparent and efficient.

One of the key takeaways from this talk: AI is not replacing humans, it is empowering them. Through automation and data analysis, advisors can save time, reduce errors and focus more on what truly matters: supporting clients and understanding their needs.

This partnership between BNP Paribas Cardif and Ploovers also highlights the importance of balancing:

⚡ the agility and innovation of a startup

🏛️ the robustness and expertise of a leading global insurer

🤝 a shared ambition to create greater value for clients

A fascinating discussion on practical, responsible and human-centered AI.

Concrete use cases throughout the customer journey

The 19th June : Michael de Toldi, Chief AI Officer at BNP Paribas Cardif, and Anthony Belpaire, Head of AI at BNP Paribas Fortis, shared concrete use cases illustrating how AI is creating value across the customer journey from KYC automation to AI-powered customer experiences.

AI is no longer just another technology feature; it is reshaping the way financial institutions operate, serve customers, fit partners needs and adapt to evolving expectations as Agentic AI is fundamentally transforming their communication and consumption patterns.

The innovation challenges of tomorrow’s insurance?

👟 The Cardif Lab’ organized several guided tours for different invited stakeholders (partners, ExCom and top management), each time offering them personalized journeys. Among these visits, one of the highlights was the one organized for collaborators’ teenagers so they could discover innovation in a fun and inspiring way.

This guided tours explored some of the most inspiring innovations shaping the future of tech, AI and customer experience. It was such an inspiring moment to connect with emerging trends already transforming insurance:

👉 generative AI

👉 agentic AI

👉 large-scale automation

👉 new digital uses redefining customer expectations and distribution models

🏆 Our Innovation Ambassadors were honored with an award in recognition of their commitment to promoting innovation at BNP Paribas Cardif, it makes it even more meaningful, as there is no better place to celebrate innovation and the people driving it forward.

Why has AI become a strategic lever for BNP Paribas Cardif?

At BNP Paribas Cardif, we are convinced that artificial intelligence is a major opportunity to accelerate our transformation, strengthen the value we bring to our partners and customers, and simplify the everyday work for our teams.

With nearly 100 AI use cases already in production, we have built strong foundations to scale further. As an insurer, our ambition is clear: to position BNP Paribas Cardif as a leading player in cutting-edge, responsible and secure AI solutions.

This transformation builds on a long-standing commitment to enhancing customer experience through technology while maintaining the highest standards to meet growing expectations.

Because the human dimension is the heart of the insurance profession, AI is seen as a powerful enabler not a replacement.

A successful and meaningful event ✨

VivaTech 2026 was the occasion for BNP Paribas Cardif to:

✅ strengthen its positioning as an actor committed to innovation

✅ develop its relationships with tech ecosystems, start-ups and partners

✅ illustrate concretely how technology can improve the customer experience

✅ inspire employees and younger generations by opening the doors to innovation

Sébastien Dessillons has been appointed head of development at BNP Paribas Cardif and joins BNP Paribas Cardif’s Executive Committee effective from 1 July 2026. As part of the transformation and development department, his mission will be to strengthen BNP Paribas Cardif’s position as a world leader in bancassurance partnerships by enhancing partner engagement, developing a value proposition that leverages the opportunities

offered by artificial intelligence and fostering innovative partnerships.

Sébastien Dessillons began his career in the public sector. He held several positions at the French Ministry of Economy and Finance, then in ministerial offices first with the Minister of Defense (2012-2014), and then with the Prime Minister (2014-2016), focusing on companies and industrial affairs.

He then joined the BNP Paribas Group in 2016, where he was responsible for the

coverage of a portfolio of major corporate clients. He later led the sector teams within the Group’s Corporate and Investment Banking division, first for Europe from 2019, then globally from 2023. In this role, he managed investment bankers specialized by economic sector and supported corporate and private equity clients in their strategic transactions, including M&A and related structured financing.

Sébastien Dessillons is a graduate of École Polytechnique (France) and is a Chief Engineer of the Corps des Mines (Paris).

BNP Paribas Cardif, the insurance company of the BNP Paribas Group, and the BCC Iccrea Group, the largest Italian cooperative banking group with 111 Credit Cooperative banks, today announced that BNP Paribas Cardif has acquired an additional 19% stake in the life insurance company BCC Vita increasing its total shareholding to 70%. The transaction falls within the framework of the agreements signed in 2023 and marks the natural evolution of a partnership that has already demonstrated solid foundations and strong results.

After BNP Paribas Cardif’s acquisition of 51% of BCC Vita, the two partners have jointly built an effective and distinctive bancassurance model, designed to meet customers’ evolving insurance needs. The additional

19% acquisition reflects a shared long-term vision and mutual trust that has been consolidated over time.

The BCC Iccrea Group network, strongly rooted throughout Italy, represents an effective distribution asset for BCC Vita, enabling it to deliver high quality insurance solutions to a broad and diversified customer base.

“This new milestone reaffirms our commitment to the BCC Iccrea Group and further strengthens BNP Paribas Cardif’s presence in the Italian life insurance market. Our partnership is built on a strong model that combines our ability to support the banking network with close collaboration between our teams and BCC Iccrea Group’s local network, helping us respond effectively to customers’ needs,” said Pauline Leclerc-Glorieux, Chief Executive Officer of BNP Paribas Cardif.

“This transaction is the concrete confirmation of the value of a strategic choice in which we deeply believe,” said Alessandro Deodato, Chief Executive Officer of BNP Paribas Cardif in Italy. “When we started the partnership in BCC Vita two years ago, we did it with a clear vision and with the intention of embarking on a stable and lasting path together. With this further acquisition, we reaffirm our long-term commitment to the BCC Iccrea Group, one of the pillars on which the growth of BNP Paribas Cardif in Italy is based”.

“We are particularly pleased with how we have launched our partnership with BNP Paribas Cardif, and today we are extending it to allow our 111 BCCs to continue offering their members and customers one of the most comprehensive and competitive ranges of products in the life insurance sector in Italy,” concluded Mauro Pastore, General Manager of the BCC Iccrea Group –.

“The development of this partnership, as set out in the agreements signed in 2023, demonstrates the soundness of the strategic plan we had devised in the interests of our BCCs, which will now have a longer timeframe to consolidate their relationships with their communities and establish themselves as a key point of reference in this sector too”.

Through this transaction, BNP Paribas Cardif reinforces its commitment to the Italian insurance market and bancassurance. It also confirms BCC Vita’s role as a strategic vehicle for business development in the life segment, thanks to the strength of the BCC Iccrea Group’s distribution network and to the daily collaboration to broaden the product offering, enhance the customer experience in an evolving market.

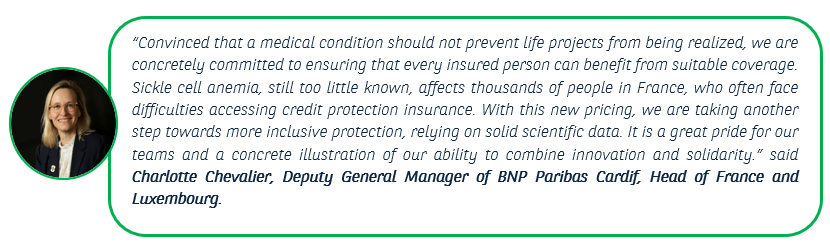

Building on its commitment to make insurance more accessible, especially for those affected by chronic or rare diseases, the insurer BNP Paribas Cardif is introducing new pricing for people with sickle cell anemia, the most common genetic disorder and the leading rare disease in France1. This advancement improves access to insurance in terms of coverage and pricing for creditor insurance contracts of BNP Paribas Cardif in France, both for clients of the BNP Paribas banking network and for brokers, wealth management advisors, and directly online via Cardif.fr

A significant step forward for the inclusion of people with sickle cell anemia

About 7.7 million people worldwide2 are affected by sickle cell anemia, a genetic disorder affecting red blood cells, representing a 40% increase in 25 years, including 30,000 people in France3. Those concerned often face difficulties accessing suitable credit protection insurance and are subject to premium surcharges on death and total and irreversible loss of autonomy guarantees, as well as significant exclusions on complementary guarantees, notably for work incapacity and disability.

Thanks to work carried out in collaboration with medical experts, BNP Paribas Cardif teams have developed a risk assessment that takes into account various therapeutic developments. This approach allows the insurer to improve pricing by more widely granting complementary guarantees and reducing surcharges. A new questionnaire is also introduced for insured people with sickle cell anemia to better understand the specifics of their condition.

When medicine advances, insurance evolves

Collaboration with the research community has enabled a better understanding of sickle cell anemia, its medical challenges, and its impact on patients’ quality of life. This initiative continues BNP Paribas Cardif’s actions for over 15 years to develop an inclusive offer, aiming to facilitate access to insurance solutions for people with rare or chronic diseases, such as inflammatory bowel diseases (IBD).

The insurer acts concretely to increase inclusion and access to creditor protection insurance. Among significant advances, BNP Paribas Cardif notably offers coverage without surcharge or exclusion to people treated for HIV, provided their viral load is undetectable at the time of subscription and to those who have overcome breast, prostate, or testicular cancer once the active therapeutic protocol is completed.

1Drépanocytose · Inserm, La science pour la santé

2 WHO issues first global guideline to improve pregnancy care for women with sickle cell disease [1] Épidémiologie de la drépanocytose en France et dans le monde | La Revue du Praticien

3 Épidémiologie de la drépanocytose en France et dans le monde | La Revue du Praticien

Joint mortgages are becoming an increasingly popular route to home ownership in Japan, but they expose couples to a structural gap: traditional mortgage CPI (Creditor Protection Insurance) typically protects only one borrower, leaving the other party’s repayments at risk if life takes an unexpected turn.

Shoichiro Fukushima, Group Leader of Promotion Planning in the Mortgage Loan Business Development Department at, Mortgage Loan business Unit at PayPay Bank, and Yasuko Yokoyama, Chief Manager in Strategic Partnership for BNP Paribas Cardif in Japan, look back on how they joined forces to fill this gap and provided PayPay Bank a highly successful entry into the very competitive Japanese mortgage market.

As a digital bank expanding into mortgages, why did you need to gain a strong foothold in this segment?

Shoichiro Fukushima (PayPay Bank) : PayPay Bank entered the mortgage market as a latecomer, so we knew that simple matching the competition or competing on price would not be enough. We needed a strong, differentiated positioning, and we believed, the most effective way to achieve this was to address the emerging social realities directly. That is why we were keen to work with BNP Paribas Cardif in Japan on the industry’s first(*). Joint Mortgage CPI, bringing a new and meaningful value proposition to mortgage customers.

What were the social issues you identified and how did it translate into a mortgage-related offer?

Shoichiro Fukushima : We observed a steady rise in joint mortgages, driven by increasing property prices and growing number of dual-income households. Yet conventional mortgage CPI typically covers only the insured borrower’s share of loan. If a serious illness such as cancer or others occurs during the repayment period, the other party’s repayments can also become difficult. We felt it was essential to provide protection to people to reduce this shared risk. The idea also came from the front line: our sales teams raised the question, whether such a product could be created, based on what they were hearing from customers.

What is joint mortgage CPI, and what makes it a first in Japan?

Yasuko Yokoyama (BNP Paribas Cardif in Japan) : A joint mortgage is a borrowing arrangement in which two or more people – typically a married couple – each take out a mortgage loan for the same property and act as joint guarantors for each other. In Japan, this structure is commonly known as a “Pair Loan”. With conventional CPI, only the insured person’s portion of loan is covered, leaving the other party’s debt unprotected. Joint mortgage CPI is the first product in Japan designed so that, if one borrower is affected by an unexpected event, the outstanding balance of both borrowers is covered together.

How does the product work in real-life scenarios for couples?

Yasuko Yokoyama :The coverage is designed to respond to a wide range of life-altering situations. If one partner dies, is diagnosed with a prescribed severe disability, or with cancer, the total outstanding balance for both parties can be reduced to zero. If a borrower is hospitalized on a repayment date due to illness or injury, the monthly repayment for both parties is covered. And if hospitalization continues for more than 12 months, the full remaining balance for both parties can also be reduced to zero.

What did each partner bring to make this possible?

Shoichiro Fukushima : We contributed the product concept, based on what we observed in the market and our understanding of the social issues our customers face. We know our customers well and we listen closely to their needs. As a digital bank, we are constantly looking for new ways to identify and address the existing gaps.

Yasuko Yokoyama : BNP Paribas Cardif in Japan with its expertise contributed in rapid co-development and in reducing the administrative burden on CPI through customized operational schemes, including responding to inquiries at call centers on weekends and direct customer response when accepting claims. We also designed a fast underwriting process supported by an automated engine, with strong focus on providing prompt and accurate responses to inquiries and consultations from the partner bank.

What early signals suggest the product is gaining traction, and what comes next?

Shoichiro Fukushima : PayPay Bank was the first in the industry to introduce joint mortgage CPI which quickly helped establish it as a reference point in this area. Since launch, the utilization rate of our joint mortgages increased by 10%, contributing directly to improved profitability. Looking ahead, with property prices continuing to rise and more young customers relying on joint mortgages, we plan to keep co-developing products that meet their evolving needs.

Yasuko Yokoyama : On our side, we are already exploring further co-development opportunities, with a clear focus on making insurance more accessible. We also place greater emphasis on stimulating CPI needs, and to continue delivering new and innovative products and solutions to support PayPay Bank’s mortgage growth.

(*) Based on research by PayPay Bank (as of March 2024)

Read more

The Innovation Ambassadors program, which includes 5 winners among 102 innovative projects submitted from 24 entities worldwide in 2025, shows that innovation can be found everywhere at

BNP Paribas Cardif!

Briefly introduce yourself

My name is Charles Druguet, I am a UX/UI Designer within the Innovation and New Business Models team at Icare. I work on all digital tools, both internal and external, intended for our partners. Icare is my first professional experience; I joined the Indicar team just before incubation at BivwAk!. I was able to design the UX and UI of the demonstrator, with the goal of making the indicators clear and useful for our clients and partners. Outside of work, I am passionate about sports, particularly rugby and boxing; and I enjoy following economic and financial news.

Hello, my name is Stéphane Leguet and I work at Icare, a subsidiary of BNP Paribas Cardif specializing in mechanical breakdown coverage and maintenance contracts for the automotive market, based in Boulogne-Billancourt near Paris in France. When I arrived in 2021, I had the chance to create the Innovation and New Business Models team. With Charles, our mission is to develop digital services that go beyond insurance, to create value for our partners and our clients.

Stéphane

Indicar was born from a simple observation: there is an expertise imbalance between professional sellers and private buyers of used vehicles. Our goal is to democratize access to technical data, such as reliability, parts prices, and risk of damages, to make private purchases safer.

Charles

Today, Indicar comes in several technical solutions for our partners, including a widget and an API. The widget integrates very quickly, in just a few hours. And the API version allows our partners to maintain control over their editorial line. Indicar is also an online demonstrator designed as a sales support tool for Icare’s sales team and our prospects.

How does your initiative correspond to the category won?

Stéphane

From the beginning, we involved the client in our process. We built Indicar in 3 key steps:

- Step 1 : After a 2-week Design Sprint, we presented mock-ups to about ten passersby on the street to validate our ideas.

- Step 2 : We created a mini-site that attracted over 4,000 visitors to test user interest and gather feedback. The conversion rate was very high, allowing us to get an internal GO to continue.

Charles

- Step 3 : We created an MVP developed in agile mode. This incubation stage at Bivwak was very intense. Every two weeks, we organized presentations for internal and external partners to share the progress of the developments, gather their feedback, and integrate their requests into the solution. This allowed us to quickly create concrete use cases, aligned with their needs.

We owe Indicar’s success to cross-functional collaboration between Icare’s Data, Marketing, and Operations teams and to the methodological expertise of the Cardif Lab team.

In summary, Indicar embodies the spirit of innovation driven by the client and the partner.

What are the next steps for your initiative?

Stéphane

After being the first widget integrated on Cardif’s API Store, Indicar’s API is now live with a partner in Portugal and we are in discussions to extend it to other partners and other regions

Charles

On the development side, we continue to refine the tool based on field feedback, to maximize its impact and adoption.

What are your tips for innovating at BNP Paribas Cardif?

Stéphane

My advice?

Find a concrete problem to solve for your clients, your partners, or your colleagues. Start small and quickly to validate your hypotheses where to focus, and find an internal sponsor who believes in your initiative.

Charles

For me, innovation at BNP and Icare goes through the involvement of all professions. It is necessary to share as much information as possible, involve as many people as possible to bring out ideas, and above all, exchange a lot. Feedback from partners and other departments brings perspectives that we do not always have internally. Sharing and collaboration are key!